Motor Vehicle Depreciation Rate As Per Income Tax Act

A Guide To Depreciation Rates As Per Income Tax For Ay 2020 21

Depreciation As Per Income Tax Act Complete List Of Depreciation Rate

Depreciation As Per Income Tax Assignment Depreciation Chart

Federal Income Tax Tables And Rates For 2014 Tax Season Aving To Invest

Rates Of Depreciation As Per Income Tax Act 1961

Depreciation Rates For Ay 2020 21 New Rates Section 32 Of Income Tax

Example a motor car was bought on 1 4 2019 for rs.

Motor vehicle depreciation rate as per income tax act.

New Higher Rate Of Depreciation On Motor Car In 2020 Motor Car Car Tax Rules

Mandatory Fees On Late Filing Of Income Tax Return For Ay 18 19 Simple Tax India

/dotdash_Final_What_Tax_Breaks_Are_Afforded_to_a_Qualifying_Widow_Nov_2020-01-c5d6697fa005491f8a0049780f7c2b82.jpg)

Ckqn5bqzgvhbkm

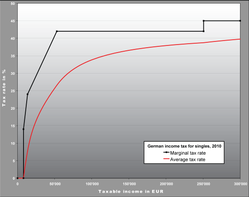

Taxation In Germany Wikipedia

Accounting Taxation Income Tax Deductions Lic Donation Mediclaim Pension Fund Home Loan Repayment Bank Fdr Etc Car Tax Deductions Income Tax Deduction

Calculation Of Depreciation Under The Income Tax Act 1961

Individual Income Tax Faq Alabama Department Of Revenue

Income From Business Or Profession Accounting Taxation Income Business Tax Refund

Hra Exemption Is Allowed On Actual Payment Of Rent Income Tax Actual Payment

2017 Income Tax Fundamentals Chapter 3 By Unicorndreams8 Issuu

Income Tax Tips Business Insurance David A Baucom

3 11 3 Individual Income Tax Returns Internal Revenue Service

Pin On Income Tax Diary

Depreciation On Buildings As Per Income Tax Law

All About Deferred Tax And Its Entry In Books

Nepal Income Tax Slab Rates For Fy 2077 78 B S 2020 21

Depreciation For Ay 2020 2021 Under Income Tax Act 1961

Income Tax Law Does Not Consider All Inherited Assets As Ancestral Property

Https Encrypted Tbn0 Gstatic Com Images Q Tbn And9gcrj3dtq6t 9ihhnsldgadpsc8fijyxwrnfoptwpoeq7bzqd8wd5 Usqp Cau

New Concessional Income Tax Rate From Fy 2020 21

Income Tax Diary In 2020 Finance Sabha Income Tax

How To Calculate Federal Income Tax 11 Steps With Pictures

Https Www Czechinvest Org Getattachment Unsere Dienstleistungen Doing Business In The Czech Republic Doing Business In The Czech Republic Taxation Cn Fs 12 Corporate Tax And Depreciation Pdf

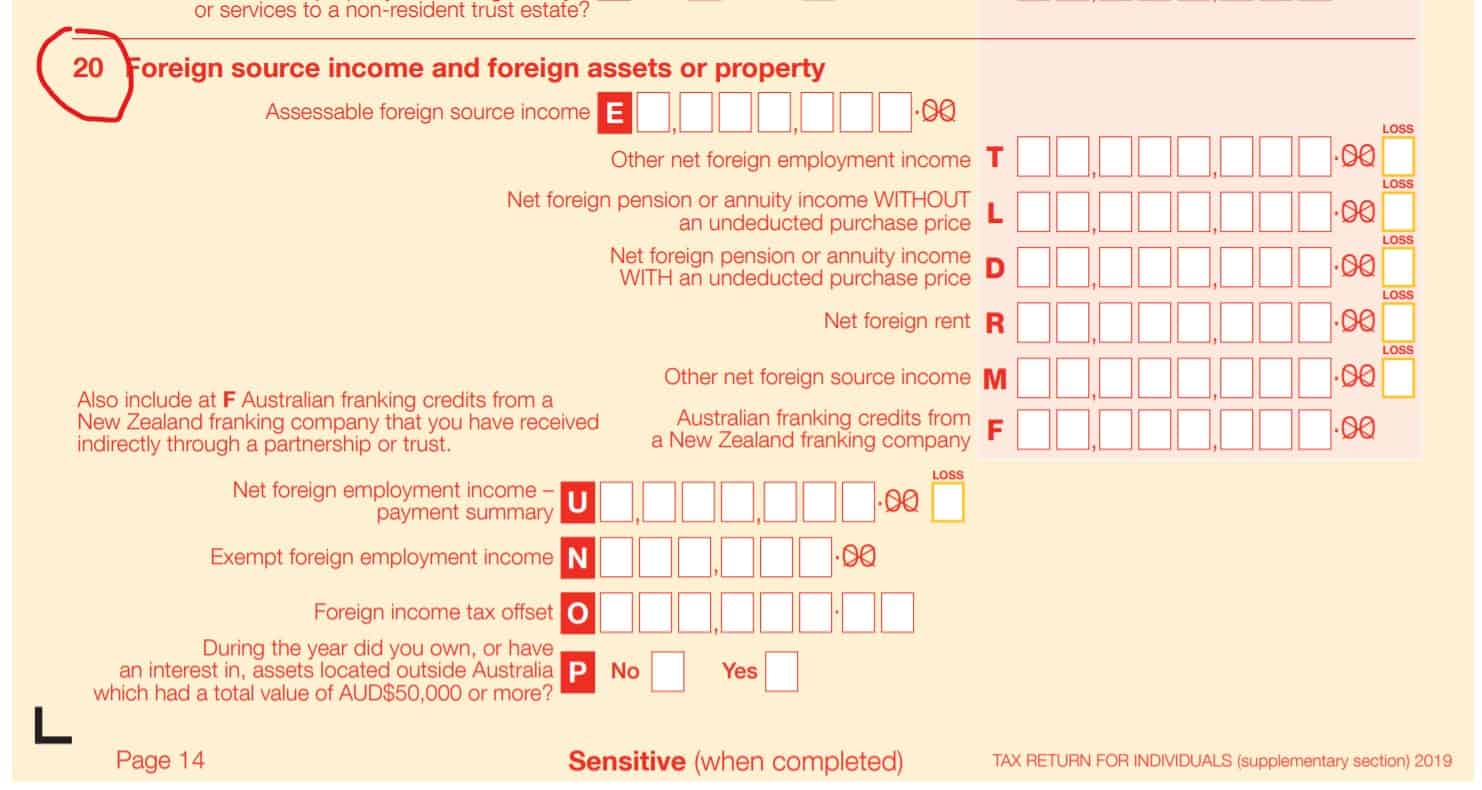

Foreign Income Tax Offset Atotaxrates Info

Source : pinterest.com